For many households, debt doesn’t come from one big decision. It builds up gradually — a credit card used for everyday expenses, a personal loan for a car or renovation, and maybe a store card that seemed convenient at the time.

Before long, you’re juggling multiple repayments, all with different interest rates and due dates. Even when you’re making every payment on time, it can feel like you’re running just to stand still.

This is where debt consolidation is sometimes considered.

What is debt consolidation?

Debt consolidation involves combining several existing debts into a single loan. In many cases, this is done by refinancing or increasing a home loan, as home loans usually have lower interest rates than personal loans or credit cards.

Instead of managing several repayments each month, you’re left with one repayment, one interest rate, and one due date — which can make finances simpler and easier to manage.

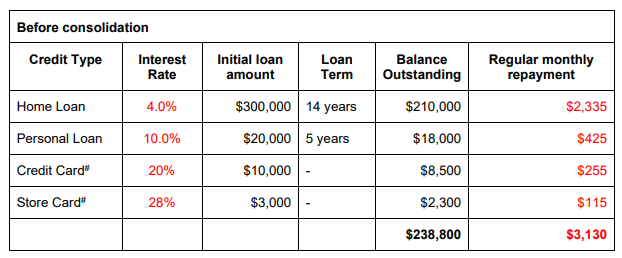

A simple example

Jenny is a good example of how quickly debts can pile up. She has a home loan, a personal loan, a credit card and a store card — each charging different interest rates and requiring separate repayments.

While Jenny is meeting her repayments, a large portion of her money is going toward high-interest debt. This makes it harder to get ahead or free up cash for other priorities.

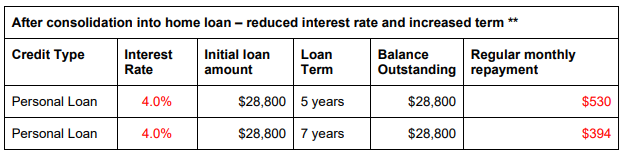

Consolidating debts to reduce interest

By consolidating her personal loan, credit card and store card into her home loan using available equity, Jenny replaces several high-interest debts with a single, lower-interest loan.

This gives her options.

Option 1: Reduce monthly repayments

Jenny could choose to lower her repayments to ease pressure on her budget.

In this scenario, Jenny could reduce her repayments by up to $401 per month, improving short-term cash flow. However, the longer loan term means the debt takes longer to fully repay.

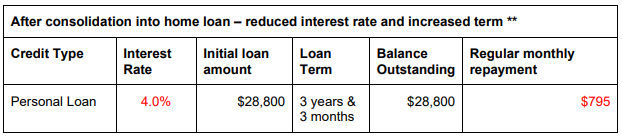

Option 2: Keep repayments the same and get debt-free sooner

Alternatively, Jenny could continue paying roughly the same amount she was paying before consolidation. This approach doesn’t reduce her monthly outgoings, but it dramatically shortens how long she carries the debt.

By maintaining higher repayments, Jenny would be free of her non-mortgage debts in just over three years.

The important trade-offs to consider

Debt consolidation can be helpful, but it isn’t suitable for everyone. Key points to think about include:

- Longer loan terms can mean paying interest for longer

- Using home equity increases the amount secured against your property

- Spending habits matter — without changes, new debts can build up again

For this reason, consolidation works best when combined with a clear plan and realistic budgeting.

Is debt consolidation right for you?

Debt consolidation can simplify repayments, reduce interest costs, or help create a clearer path out of debt — but the right approach depends on your circumstances and goals.

A licensed financial adviser can help you understand whether this strategy suits your situation and how it may affect your long-term financial position.

Sometimes, the biggest benefit isn’t just the numbers — it’s the peace of mind that comes from having one clear plan instead of four competing debts.

If you’d like guidance tailored to your circumstances, speaking with one of our financial advisers can help you move forward with greater clarity and confidence.

| The information provided in this article is general in nature only and does not constitute personal financial advice. |