Interest rates are rising, and the Reserve Bank of Australia (RBA) has hinted that they could stay elevated for longer than expected.

While people who live off their investments, including self-funded retirees, welcome the rise, homebuyers must think about what higher rates will mean for them, especially if those rates stay higher for longer.

Many households put their lifestyles and financial decisions on hold until rates eventually start to come down – notably those who are looking to buy a home.

This might seem the wisest strategy, but can in fact, be financially risky. For example, property prices are often lower during periods of high interest rates. This means that buying at this time may mean borrowing less, which, over the course of a 20 – 30 year mortgage, could see borrowers potentially save $000s.

If you already have a mortgage, the government’s Moneysmart website recommends you review it at least every year. This is not just to identify any features and benefits your lender offers that you may not have considered, but to keep abreast of other lenders’ deals that may work better for you, particularly when interest rates are on the rise.

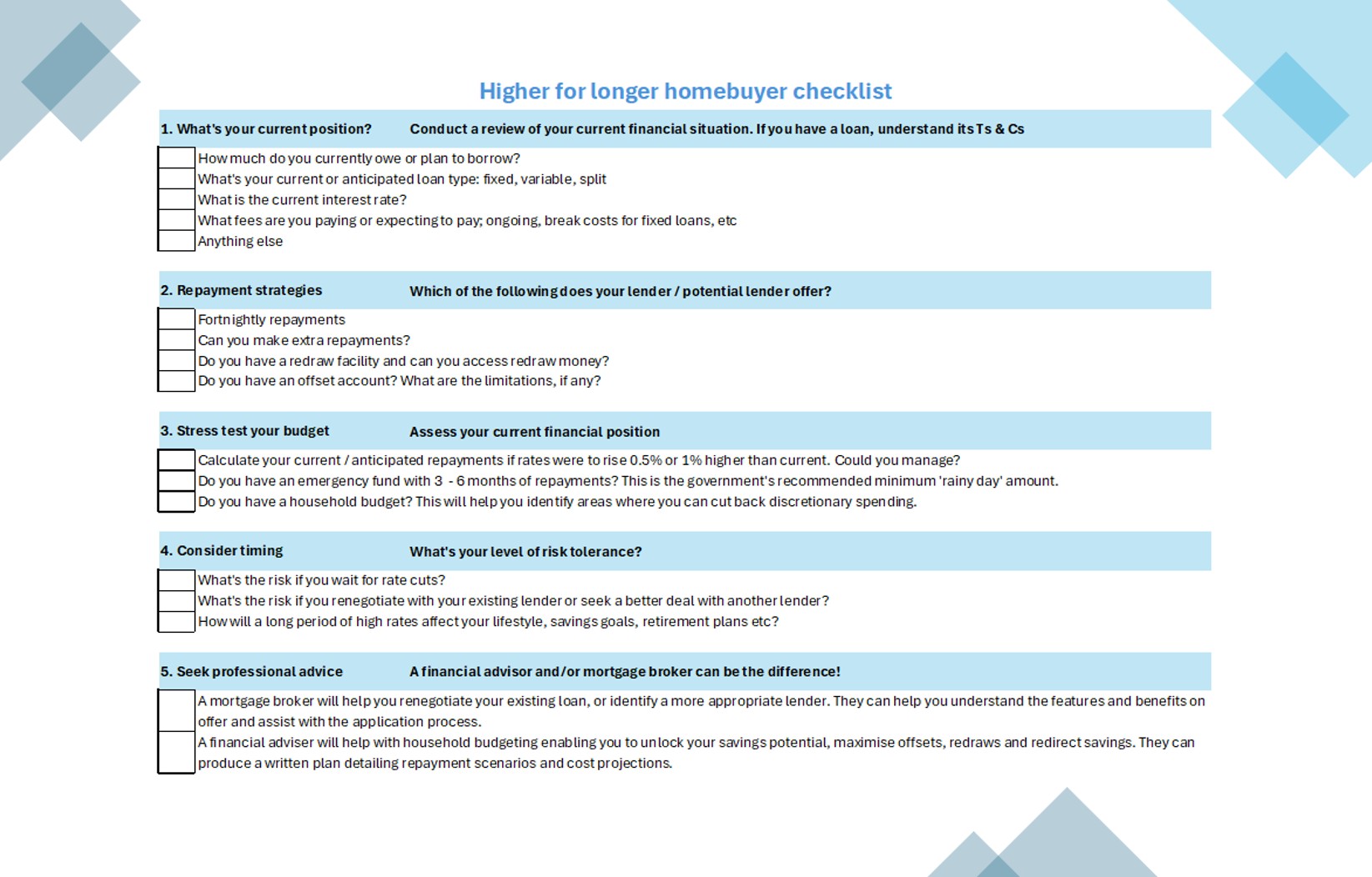

We’ve put together a five-point checklist you can use to evaluate your financial position in relation to your current, or future, housing loan. Some of these points you may have already considered, others you may not have. But as we buckle-up in preparation for what could be higher-for-longer rates, it’s worth taking a look.

According to a 2025 survey conducted by Finder.com.au, over the previous two years, 28% of Australians abandoned plans to buy a property due to high interest rates.

Naturally, one of the greatest concerns associated with investments is timing the purchase and/or sale. The real estate market is no exception.

While the reality of higher-for-longer rates can be daunting, and it’s understandable that so many homebuyers are leaning towards playing it safe, it is possible to remove some of the fear factor.

Take control by consulting a professional who will help you understand your options, reduce uncertainty and run the sums to see how you can still achieve your financial goals.

Bottom line: whether you choose to wait for rates to drop or you decide to act anyway, making uninformed decisions is never a good strategy.

And remember, it’s not always about the interest rate itself, it’s how you work with it!