The superannuation rules have become simpler and more generous over the years, but understanding what they mean for you can still seem confusing.

Here is a simple explanation of super contributions. Just refer to the table below for specific details and read further for a longer explanation under the age group that relates to you.

Major types of super contributions

Firstly, a quick explanation of the different types of super contributions available:

-

Super Guarantee (SG)

Employers must pay the superannuation guarantee for their employees, currently set at 11.5% p.a. of the employee’s earnings. This will rise to 12% from 1st July 2025, but following that there are no further increases planned.

-

Pre-tax contributions

You can make additional voluntary contributions deducted from your salary by your employer, thus reducing your taxable income. These are classed as concessional contributions, and are currently capped at $30,000 per year. However, if you have unused cap amounts from previous years, you may be able to carry them forward to increase your contribution caps in later years. Concessional contributions are taxed at only 15% when received into your super fund.

-

Personal contributions

Personal contributions for which you do not claim a tax deduction are classed as non-concessional contributions. You can contribute a maximum of $120,000 per year, but you may be eligible for a bring-forward arrangement allowing you to make up to three years’ worth of contributions in the first year of a three-year period.

-

Government co-contributions

Subject to restrictions on your annual income, if you make a personal contribution to your super, the government may make an additional contribution of up to $500 per year.

-

Spouse contributions

You may be able to claim a tax offset against your own income if you make a contribution to your spouse’s super.

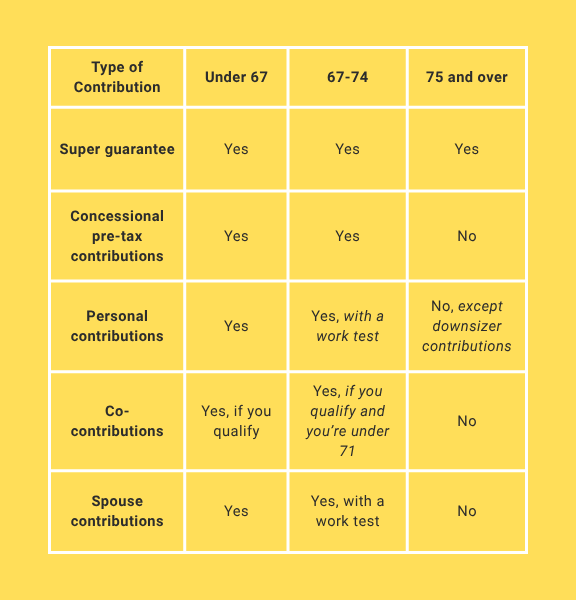

Age eligibility for super contributions

In more detail . . .

If you are under 67

The rules are simple. You can make or receive any type of contribution described above.

However, the government co-contribution is targeted at low to middle income earners so not everyone qualifies. To receive any co-contribution, you must earn at least 10% of your income from employment, including self-employment, have income of less than $62,488 p.a. and make a personal contribution. When you lodge your tax return, the ATO will calculate your co-contribution (maximum $500) and pay it into your fund.

If you make a contribution for your spouse, he or she must meet the under-75 age requirement and earn less than $40,000. For a contribution of $3,000 the contributing spouse can receive up to an 18% tax offset, knocking up to $540 off their tax.

Workers with income of less than $37,000 may receive a government contribution of up to $500 to their superannuation savings through the Low-Income Super Tax Offset (LISTO). This is to offset the 15% contributions tax paid by the fund on a low-income earner’s contributions and aims to ensure they pay no tax on SG contributions.

If you are 67 to 74

If you are working, your employer will still pay the superannuation guarantee and you can make extra contributions such as salary sacrifice. However, to make a personal contribution or receive a contribution from your spouse, you need to be working.

The work test is not difficult to satisfy. Sometime in the financial year, you must be gainfully employed (earning money) for 40 hours over any 30-day period. You could do it all in one week or work ten hours a week for four weeks.

If you are 75 or over

You can receive the superannuation guarantee (SG) and also make personal contributions funded from selling your home and downsizing (‘downsizer contribution’).

Professional advice will help you maximise the benefits of your super contributions

If you want to make sure your super contributions are working as well as they could for your future, make an appointment with our team for a no-obligation chat to discuss the ultimate way to secure your financial future.

| The information provided in this article is general in nature only and does not constitute personal financial advice. |