Here are some key opportunities to consider leading up to 30 June.

Overview

With the end of financial year (EOFY) approaching, now is a great time think about actions you could be taking before 30 June to build wealth tax-effectively.

As per previous EOFYs, key priorities are likely to be:

▪ maximising super contributions without exceeding the relevant caps

▪ bringing forward deductible expenses

▪ deferring taxable income, and

▪ managing capital gains.

This article outlines the key opportunities and issues to consider before 30 June this year

Concessional super contributions

Use surplus cashflow or savings to benefit from making additional concessional contributions (CCs) up to the available CC cap.

Options to consider are making personal deductible contributions (PDCs) and/or, if an eligible employee, arranging to sacrifice pre-tax salary into super.

The CC cap is $25,000 in 2019/20. However, some may be eligible to contribute more than $25,000 in 2019/20 without exceeding the cap by making ‘catch-up’ CCs. To do this, they needed to have made CCs of less than the $25,000 cap in 2018/19 and had a total super balance of less than $500,000 on 30 June 2019. The usual contribution eligibility rules also apply.

Salary sacrifice or PDCs

Where you have a choice of salary sacrifice and PDCs, some key things to keep in mind are:

- although the timing of cashflows and key tax events are quite different, the net benefit is generally similar

- you can only salary sacrifice income not already earned, which is likely to limit the amount that can be contributed in the lead up to EOFY, and

- PDCs offer more flexibility and control, which may appeal to those wanting to contribute capital from a range of sources or make a ‘top-up’ contribution at EOFY to take full advantage of the CC cap.

CC cap considerations

When seeking to maximise the CC cap in 2019/20, it’s important to review contributions made in 2018/19 (if planning to make catch-up contributions) and contributions already made this financial year.

Remember that CCs include all employer contributions (i.e. SG contributions are also included, not just salary sacrifice), PDCs and certain other amounts. Some other key things to look out for are:

- contributions may be made to more than one fund

- SG contributions could end up higher than anticipated due to a pay rise or a bonus

- there may be time lags between when salary is earned and the related salary sacrifice contribution is made to the fund (e.g. SG payments that were made to a super fund in July 2019 that related to employment in late 2018/19 will count towards the 2019/20 CC cap), and

- contributions need to be received by the fund before 30 June to count towards the 2019/20 caps

A note on super contribution deadlines

For those wanting to make additional super contribution this financial year must do so before 30 June 2020 to ensure they count towards the 2019/20 caps.

As a general guide, a super contribution is made when it is received by the super fund. For example, if someone is contributing electronically via BPAY, the contribution is deemed to have been made when the funds are credited to the super account, not the day the you make the BPAY transaction.

Individual super funds may also have specific requirements and deadlines that need to be taken into account when making super contributions towards the EOFY.

Notice of intent

For those who want to claim a deduction for personal super contributions need to make sure they lodge a ‘Notice of Intent’ form with the super fund by the earlier of the:

▪ date the tax return is lodged for the year the contribution was made, or

▪ end of the financial year following the financial year in which the contribution was made.

A notice of intent cannot be accepted by the fund if:

▪ you have exited the fund

▪ contribution(s) being claimed have been paid out as a lump sum or used to start a

pension, or

▪ you have already submitted a contributions-splitting application that has been accepted

by the fund.

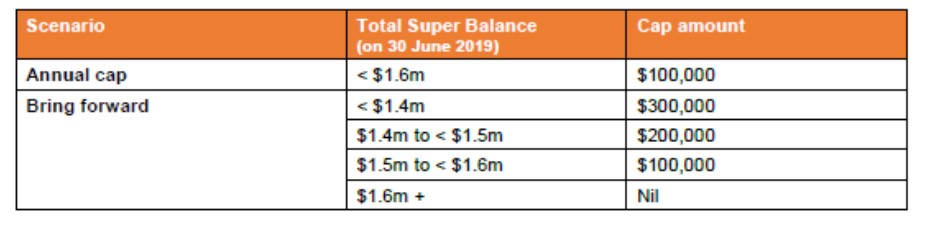

Non-concessional super contributions

You may want to make non-concessional contributions (NCCs) up to the relevant NCC cap before the EOFY. When doing this, it’s important that the contribution is received by the fund before 30 June 2020.

You need to also be careful if your superannuation balance is around $1.6 million and you need to check your contributions for the previous two financial years.

It’s essential to review all NCCs made in 2019/20, as well as the two previous financial years to see whether a bring forward was triggered by contributing more than the annual cap.

NCC cap

The table below summarises the NCC cap that may be available in 2019/20 in different scenarios.

Co-contributions

If lower income person who earn at least 10% of their income from employment or carrying on a business make an NCC, may be eligible for a Government co-contribution of up to $500. In 2019/20, the maximum co-contribution is available if they contribute $1,000 and earn $38,564 or less. A lower amount may be received if they contribute less than $1,000 and/or earn between $38,565 and $53,563.

Spouse contributions

You may be eligible for a tax offset of up to $540 on super contributions of up to $3,000 they make on behalf of their spouse if their spouse’s income is $37,000 pa or less. The offset gradually reduces for incomes above $37,000 pa and completely phases out at $40,000 pa or more.

Minimum pension payments

Those who have account-based income streams must receive at least the minimum pension payment before the EOFY. However, a minimum payment does not need to be made if the account-based income stream is commenced between 1 June and 30 June. Also, a pro-rata minimum payment is required if commenced between 1 July 2019 and 1 June 2020.

Utilise instant asset write-off scheme

Under the current scheme, small businesses with a turnover of less than $50 million may be able to claim a full upfront tax deduction of up to $30,000 when purchasing eligible depreciating assets in the 2019/20 financial year.

Pre-paying expenses

Pre-paying deductible expenses can bring forward the tax deduction and reduce assessable income.

Examples include:

- paying final quarter SG contributions before 30 June (payment deadline is 28 July 2020)

- pre-paying up to 12 months premiums on an income protection policy held outside super, and

- pre-paying 12 months interest on a fixed rate investment loan.

Managing capital gains

By selling assets that trigger a capital loss, the loss can be used to offset capital gains realised this financial year. Make sure you don’t breach the ‘wash sale’ provisions. It should be appropriate to sell that asset.

Another strategy to consider is deferring the sale of assets that would give rise to a capital gain until a future financial year. This defers paying capital gains tax (CGT). This could also reduce the CGT payable if your taxable income is sufficiently lower in the future financial year (egg you have retired) and/or you qualify for the general 50% CGT discount by extending the period of ownership beyond 12 months.

Note: In the 2019 Federal Budget, it was proposed that the superannuation contributions work test will no longer need to be met to make voluntary contributions from 1 July 2020 for those aged 65 and 66. At the time of publishing this article, legislation had not been introduced. If introduced and passed, this could have implications for those planning to make personal super contributions in 2019/20 and beyond – particularly those contemplating triggering the bring forward rules when making non-concessional contributions and making catch-up concessional contributions. We will issue an update when there are further developments