This year’s Federal Budget includes a mix of measures that impact tax, housing, investments and everyday costs. While some changes may create opportunities, others may mean it’s worth reviewing existing plans and strategies.

Note: Many of these measures are proposals only and may change before becoming law (unless stated otherwise).

Investment and property changes

Capital gains tax (CGT) reforms

From 1 July 2027

Key changes:

- The 50% CGT discount will be replaced with indexation (inflation adjustment) for gains made from 1 July 2027

- A minimum 30% tax rate will apply to capital gains

- Applies to assets like property and shares held by individuals, trusts and partnerships

What this means for you

Future investment gains may be taxed differently, depending on inflation and your marginal tax rate.

Example

If an asset grows in value, only the gain above inflation may be taxed, but at a minimum 30% rate.

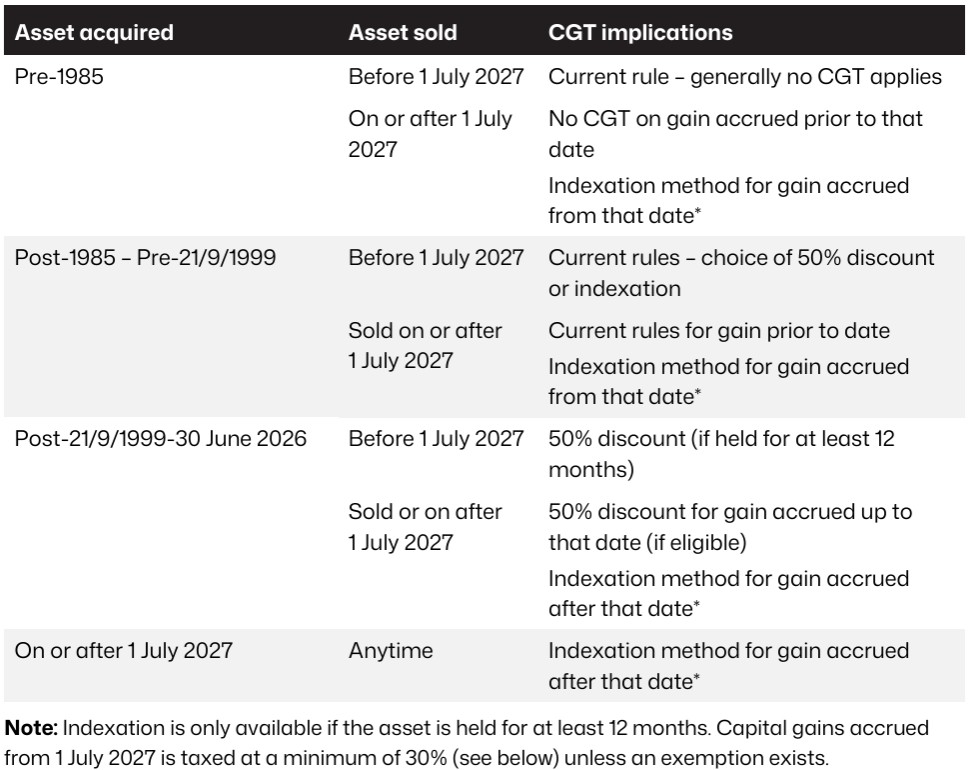

A summary of the CGT treatment based on acquisition date is below

Minimum 30% tax on capital gains

A minimum tax rate of 30% will apply to real capital gains accrued from 1 July 2027. Those already paying tax at 30% or more would not be further impacted by the minimum tax.

An exception applies for people receiving a means-tested income support payment, such as Age Pension or JobSeeker Payment, in the income year the gain is realised. In these cases, the capital gain would continue to be taxed at the individual’s marginal tax rate rather than being subject to the 30% minimum tax.

Exclusions

A number of exclusions apply to these changes, including:

- companies and super funds (including SMSFs) are not impacted by these changes and gains continue to be taxed under current rules, and

- no changes to the main residence exemption and small business CGT concessions.

Investors in newly built residential property can choose between retaining the current 50% CGT discount or applying the new CPI-indexation method with the minimum 30% tax (see above).

Example 1 – transitional arrangements

John bought an established property on 1 July 2017 for $500,000 and sells it on 1 July 2032 for $1 million. The property is worth $800,000 on 1 July 2027.

Under the proposal, the gain from 1 July 2017 to 30 June 2027 would continue to be assessed the current CGT rules, including the 50% discount.

Taxable capital gain using 50% method (1 July 2017 to 1 July 2027):

= 50% x ($800,000 less $500,000)

= $150,000 (The minimum tax of 30% does not apply to this amount)

The gain from 1 July 2027 to 1 July 2032 would be assessed under the new indexation method, using $800,000 as the starting cost base for that period.

Taxable capital gain using indexation method (1 July 2027 to 1 July 2032):

= $1m less indexed cost base of $800,000 using future CPI indexation

If John is not receiving a means-tested income support payment in the year of sale, the minimum 30% tax could apply to the post-1 July 2027 component of the gain.

Example 2 – minimum tax

Jack has a taxable income before capital gains of $25,000 in 2029/30 and realises a capital gain of $10,000 on an asset that he purchased in 2027/28. Jack does not receive an income support payment so is not exempt from the minimum 30% tax rate.

The tax on Jack’s capital gain of $10,000 is $1,400, or a tax rate of 14% (excluding the Medicare levy). As this is lower than 30%, Jack pays an additional $1,600 in tax to bring the tax rate on his capital gain up to 30%. Jack may have tax offsets available to reduce the minimum tax and would be exempt from the minimum tax if he received an income support payment in that year.

TIP

The proposal may reduce the relative attractiveness of investing in growth assets held under an individual’s name. Shares with franking credits may become more favourable. Furthermore, the changes may favour other strategies, including super, investment bonds and debt reduction.

People may wish to review ownership structures across super, personal names, trusts and companies, and whether the asset location remains appropriate.

Depending on your objectives and risk profile, it may be worth considering whether growth assets are better held in super and more defensive assets outside super. Those with pre-1985 assets may also wish to review whether action should be taken before 1 July 2027, given the proposal would remove the full exemption for future gains from that date. It may also be worth revisiting dividend reinvestment plans and dollar-cost averaging arrangements. While these strategies may still be appropriate, any new parcels acquired from 1 July 2027 could be subject to the new CGT methodology.

Negative gearing changes

From 1 July 2027

- For established properties purchased after 12 May 2026:

- Losses can no longer reduce other income (e.g. salary)

- Instead, losses can only offset rental income or capital gains from property

- New builds are generally excluded from these restrictions

- Other asset classes, such as shares or commercial property, are not affected.

- Given that SMSFs are exempt from these changes, it will be interesting to see whether this results in a shift away from holding established residential properties in individual names towards investment via an SMSF under an LRBA.

What this means for you

The Government has announced it will limit negative gearing for residential property to new builds. From 1 July 2027, losses from established residential properties will only be deductible against rental income or the capital gains from residential properties. Excess losses will be carried forward and are able to be offset against residential property income in future years. These changes will apply to individuals, partnerships, companies and most trusts.

Transitional rules

For established residential properties:

- Properties held at announcement (including contracts entered into but not yet settled) will be exempt from the changes until disposed of.

- Properties purchased between the announcement and 30 June 2027 may be negatively geared during this period, but not from 1 July 2027.

- Properties purchased from 1 July 2027 will not be able to be negatively geared.

Example

If your rental property makes a loss, you may need to carry that loss forward rather than offsetting it against your salary.

Key tip

- Existing properties held before the change are generally unaffected.

Negative gearing is where the costs of owning an investment property, such as loan interest and other expenses and deductions, are higher than the rent it brings in. Existing holdings and eligible new builds continue to receive the current treatment.

An eligible new build generally means a property that genuinely adds to housing supply, such as a newly built dwelling on vacant land or a development that increases the number of homes.

Cost of living and tax relief

Working Australians Tax Offset (WATO)

From 1 July 2027

- A new tax offset of up to $250 per year for people earning income from work

- Applies to wages, salary and some business income (e.g. sole traders)

What this means for you

This reduces the amount of tax you pay (rather than your taxable income).

Key tip

- The offset is expected to apply automatically through your tax return.

Lower income tax rates

From 1 July 2026 and 1 July 2027

- The lowest tax rate (for income between $18,201 and $45,000) will reduce:

- From 16% to 15% from 1 July 2026

- Then to 14% from 1 July 2027

What this means for you

You may pay slightly less tax on your income.

Key tip

- These changes are already legislated and apply automatically.

- The actual benefit depends on your income level.

$1,000 instant tax deduction

From 2026–27 income year

- Employees can claim a standard deduction of up to $1,000 for work-related expenses

- No receipts required if claiming up to $1,000

- If expenses exceed $1,000, full records are still required

What this means for you

Tax time may be simpler if you have modest work expenses.

Example

If you spend $600 on work-related items, you can claim $1,000 without itemising.

Key tip

- You can still claim actual expenses if they exceed $1,000, so keeping receipts may still be useful.

Medicare levy threshold increase

For 2025–26 financial year

- Low-income thresholds increase by 2.9%

- More people may pay a reduced Medicare levy or none at all

What this means for you

Lower-income households may pay less tax overall.

Key tip

- This is most relevant if your income is close to the threshold.

Superannuation

Low Income Superannuation Tax Offset (LISTO) expansion

From 1 July 2027

- Income threshold increases from $37,000 to $45,000

- Maximum offset increases from $500 to $810

What this means for you

More low‑income earners may receive a refund of contributions tax paid into super.

Key tip

- Ensure your super fund has your tax file number and your tax return is lodged.

Health and insurance

Private health insurance rebate changes

From 1 April 2027

- Age-based higher rebates will be removed

- All age groups will receive the same base rebate (income-tested)

What this means for you

Some older Australians may pay higher premiums.

Key tip

- Review your cover at renewal and understand any long-term implications of changes.

- The proposed changes mean higher premiums for older Australians, which may impact those on low income, particularly Age Pensioners and retirees. For some already managing cost-of-living pressures, this could lead to downgrading or cancelling private health insurance altogether, even though older Australians are more likely to need timely medical care. In some cases, taking out private health insurance again in the future could result in a Lifetime Health Cover loading which increases premiums. Changes to cover may also affect the types of policies or benefits available when you return, so it’s worth considering both short-term savings and longer-term costs.

Government support and social security

Pension Supplement changes (overseas travel)

From 20 September 2026

- Full Pension Supplement paid for up to 12 weeks overseas (previously 6 weeks)

- Stops after 12 weeks or if living overseas permanently

What this means for you

Short-term travel may have less impact, but extended stays could reduce payments.

NDIS reforms

From 2026 onwards (phased)

- Stronger fraud controls and provider oversight

- Changes to eligibility and assessment processes

- Greater focus on people with permanent and significant disability

What this means for you

The system may become more structured, with tighter eligibility and review processes over time.

Aged care and home support

Support at Home changes

From 1 October 2026

- Personal care services (e.g. showering, dressing) will be fully government funded

- More packages will be available

What this means for you

Out-of-pocket costs for some in‑home services may reduce.

Example

If you receive personal care at home, you may no longer pay for those services.

Key tip

- Other services may still require co‑payments depending on your income and assets.

Residential aged care funding

From 1 July 2026

- Increased funding to expand the number of aged care beds

- Incentives for providers to improve facilities and support low‑means residents

What this means for you

There may be more availability and improved quality of residential care over time.

Final thoughts

This year’s Budget introduces a mix of tax reforms, cost‑of‑living relief and changes to support systems. Some measures apply soon (such as tax cuts), while others are proposed to begin over the next few years.

Key reminder:

Many measures are proposals only and may change before becoming law.

If you would like to understand how these changes relate to your personal situation, speaking with us can help bring clarity.

Other Proposals

Minimum tax on discretionary trusts

From 1 July 2028

- A minimum tax rate of 30% will apply to discretionary trust income

Exemptions

The Government has confirmed the minimum tax will not apply to other types of trusts such as:

- fixed and widely held trusts (including fixed testamentary trusts)

- complying superannuation funds,

- special disability trusts,

- deceased estates, and

- charitable trusts.

In addition, some types of income such as primary production income, certain income relating to vulnerable minors, amounts to which non-resident withholding tax applies, and income from assets of discretionary testamentary trusts existing at announcement will also be excluded.

What this means for you

There may be less flexibility in distributing income to lower‑tax family members.

Key tip

- A three-year window from 1 July 2027 allows some restructuring options.

Small business instant asset write-off extension

From 1 July 2026

The instant asset write-off threshold of $20,000 will be made permanent. The threshold was set to reduce to $1,000 from 1 July 2026. Small businesses with aggregated annual turnover below $10 million can immediately deduct the full cost of eligible assets costing less than $20,000. The threshold applies on a per asset basis. Assets valued at $20,000 or more can continue to be placed into a depreciation pool and depreciated at 15% in the first income year and 30% thereafter.

Electric vehicle (EV) tax concession changes

From 1 April 2027

- FBT exemption for EVs will be scaled back in stages

- Higher-priced vehicles will lose some tax concessions over time

What this means for you

The tax benefit of salary packaging an EV may reduce in future years.

Key tip

- Existing arrangements generally keep their current treatment.

Other super measures (already legislated)

- Payday super – contributions to be paid within 7 business days of payday from 1 July 2026

- Division 296 tax – additional tax on earnings for balances above $3 million from 1 July 2026

What this means for you

These measures mainly affect how and when super contributions and taxes apply.

1 thought on “Priority1 2026 Federal Budget Update – Insights and things you need to consider”

A most useful presentation of the changes which will affect our future liabilities. Thank you Corin.

Comments are closed.